How can insurance companies charge customers low premiums?

We know that individuals plan for the future and make investment decisions to achieve their long-term financial goals. But these plans may be interrupted by certain events which can have negative financial consequences. Examples of such events include the person’s premature death, critical illness such as cancer or damage to his/her property from fire.

We know that individuals plan for the future and make investment decisions to achieve their long-term financial goals. But these plans may be interrupted by certain events which can have negative financial consequences. Examples of such events include the person’s premature death, critical illness such as cancer or damage to his/her property from fire.

By buying insurance, the individual transfers the possibility of large uncertain financial losses to the insurer in exchange for paying a relatively small certain premium. If the insured event occurs, then the insurer will make a payment to the policyholder that covers all or part of his/her financial loss.

Simply, insurance provides protection for the individual from unexpected events.

How does an insurer deal with the possibility of having to make large payments to policyholders?

The answer to this key question involves an important principle that lies at the heart of how insurance works. This principle is called risk pooling.

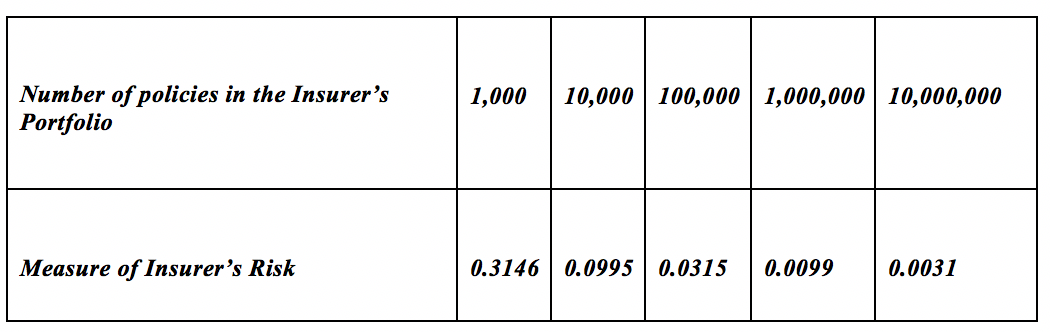

Risk pooling means the spreading of risks. Simply put, risk pooling spreads the cost of losses from some policyholders among a larger group of policyholders. Hence, we may conclude that the larger the group, the lower the risk for the insurer.

For this reason, it is said that insurers prefer to have a large number of policies in its insurance portfolio

Here is an illustration of the principle of risk pooling for the case where the probability of a loss is one per cent.

We see that the insurer’s risk declines towards a zero value as the number of policies is increased.

Key Takeaway

Our key takeaway is best summarised by the Examination Committee of the Society of Actuaries (2005) which we restate as follows:

For a very large number of policies, the insurer’s risk tends to zero.

Caution

We emphasise that the principle of pooling is not effective when a single event causes a large number of claims. Examples of such events are epidemics, terrorism and weather-related multiple automobile accidents.

Do you want to find out more about this and related principles of insurance? Download our eBook “Principles of Insurance” Dr. Abdul Rahman and Dr. Dick Harryvan. You can also follow Dr. Rahman on Twitter at @AHRahman88